A report by NKP | M&A Insights - Website Edition

Mapping valuation dynamics and emerging opportunities across Infrastructure Services platforms

Updated: 2 June 2026

This subscriber edition maps valuation outcomes and consolidation dynamics across European Infrastructure Services platforms, with a particular focus on Northern Europe (the UK, DACH, Benelux, and the Nordics), and highlights where M&A activity is currently forming.

Based on a set of observed transactions from 2021–2026 and NKP | M&A Insights’ proprietary tracking of emerging situations, the report shows why Infrastructure Services should not be treated as a single valuation category. Multiples vary materially depending on whether a business is exposed to recurring maintenance, framework-based revenue, regulated customers, technical specialisation, structural infrastructure investment themes, and scalable delivery models.

Across the transactions analysed, observed EV/EBITDA outcomes range from approximately 6x to the high-teens, with most scaled infrastructure services platforms clustering around 8x–12x. Higher valuation outcomes are typically associated with businesses benefiting from strong infrastructure criticality, technical differentiation, margin quality, customer embeddedness, and exposure to growth themes such as electrification, grid investment, telecom infrastructure, water and wastewater renewal, rail investment, and renewable energy services.

The analysis is intended to support investors and advisors in understanding current valuation benchmarks, ownership dynamics, buyer appetite, and the forward pipeline of potential opportunities as currently observed as of 31 May 2026.

NKP | M&A Insights provides proprietary, validated, early-stage M&A intelligence across Northern Europe - surfacing and contextualising non-public ownership and transaction dynamics, often months before formal processes emerge and broader market visibility.

Subscribers receive a daily curated intelligence feed, continuous tracking of emerging and live situations, and embedded cross-border context on combination opportunities, valuation levels, and buyer mappings. On average, we surface 5–7 new situations daily, most of which are not covered by traditional M&A platforms, and typically months before broader market visibility.

Trusted by 200+ private equity and advisory teams, NKP acts as an intelligence infrastructure layer to reduce information asymmetry and strengthen origination and competitive positioning.

The situations referenced in this report draw on this intelligence base and are intended to provide additional forward-looking context alongside the valuation analysis presented herein.

For the purpose of this analysis, Infrastructure Services platforms refer to businesses that provide hands-on technical services required to build, install, maintain, repair, upgrade, refurbish, renovate, and operate physical infrastructure assets.

These platforms typically serve end-markets such as utilities, energy networks, power and grid infrastructure, telecom infrastructure, transport infrastructure, water and wastewater systems, renewable energy infrastructure, public infrastructure, industrial facilities, data centres, and other mission-critical asset bases where uptime, reliability, capacity expansion, safety, and lifecycle performance are critical.

The category is defined by active service delivery to the asset base: work that physically creates, modifies, repairs, extends, or maintains infrastructure. It therefore excludes standalone Testing, Inspection, Certification, and Compliance providers, where the core activity is to inspect, test, certify, or verify assets without materially changing the physical asset itself.

This includes providers offering:

The defining characteristic across these platforms is that services are delivered directly to physical infrastructure assets and involve hands-on work that constructs, installs, maintains, repairs, upgrades, refurbishes, or extends those assets. While many Infrastructure Services platforms benefit from recurring maintenance, framework agreements, or long-term customer relationships, recurrence is not a strict requirement. Project-based or greenfield work can also fall within the scope of this analysis where it is directly tied to critical infrastructure assets, such as utility networks, telecom infrastructure, transport systems, energy infrastructure, water and wastewater assets, renewable energy projects, data centres, and other mission-critical physical infrastructure.

This analysis does not include:

The category is therefore best understood not as a single end-market, but as a group of technical service models united by asset criticality, regulatory relevance, and customer reliance on specialist external providers. This distinction is important when assessing valuation outcomes, as Infrastructure Services platforms can differ materially by contract structure, end-market exposure, technical specialisation, labour intensity, regulatory complexity, and scalability.

Buyer interest in Infrastructure Services platforms is supported by the essential nature of the underlying assets they serve. Utilities, energy networks, telecom infrastructure, transport systems, public infrastructure, industrial facilities, and critical built environments all require specialist engineering and construction capabilities plus ongoing maintenance, inspection, repair, testing, compliance, and lifecycle support to remain safe, operational, and compliant.

These services are often difficult for customers to defer. Infrastructure owners and operators face uptime requirements, regulatory obligations, safety standards, ageing asset bases, and growing investment needs linked to energy transition, electrification, connectivity, and public infrastructure renewal. This creates a demand profile that is typically more resilient than many discretionary B2B services.

From an acquirer and investor perspective, this typically translates into:

Many platforms have also evolved from narrower maintenance or field-service providers into broader infrastructure lifecycle support partners, combining construction support, installation, repair, refurbishment, upgrade works, planned maintenance, emergency response, and operational field services. This can increase wallet share, deepen customer relationships, and create scope for operational leverage as the platform scales.

Well-positioned Infrastructure Services platforms therefore often combine resilience, recurring demand, technical differentiation, and buy-and-build potential, making them attractive to both financial sponsors and strategic consolidators.

Infrastructure Services is not a single, uniform market. The sector spans a broad range of technical service models, end-market exposures, contract structures, and delivery requirements. The most important distinctions are not only between utilities, telecom, transport, energy, data centre, and industrial infrastructure, but between project-led delivery, recurring asset maintenance, regulated asset renewal, and broader lifecycle service platforms.

At one end of the market are local and regional technical service providers focused on maintenance, repair, and emergency response for specific infrastructure assets. These businesses often benefit from recurring demand and strong customer proximity, but may remain labour-intensive, locally anchored, and dependent on operational capacity, field technician availability, and customer relationships in specific geographies.

A second group consists of specialist infrastructure construction and installation contractors delivering hands-on work across power and grid infrastructure, telecom networks, transport infrastructure, water and wastewater systems, renewable energy assets, data centres, and other mission-critical infrastructure. These providers are differentiated from generic contractors by technical specialisation, asset-specific know-how, and direct relationships with infrastructure owners or operators.

A third category includes broader infrastructure lifecycle service platforms. These businesses combine planned maintenance, repair, installation, refurbishment, network expansion, and operational support across multiple asset types or end-markets. They often have deeper customer relationships, larger framework agreements, and greater scope for cross-sell, making them more relevant as consolidation platforms.

Finally, technology-enabled and data-led infrastructure services providers form an increasingly distinct segment. These operators use software, remote monitoring, predictive maintenance, workflow tools, asset data, and automation to improve service delivery, reduce downtime, and support more proactive infrastructure management. Where technology changes delivery economics and strengthens customer embeddedness, these businesses can differ materially from traditional field-service models.

Understanding where a company sits across this spectrum is critical to interpreting valuation outcomes. Infrastructure Services platforms can vary significantly in their revenue visibility, contract quality, exposure to regulated infrastructure end-markets, technical specialisation, labour intensity, scalability, and ability to consolidate fragmented local markets.

Transaction details, valuation metrics, and supporting context are available to NKP subscribers.

Given the mix of scaled network services platforms, specialist technical operators, and smaller locally anchored infrastructure services businesses, valuation references are presented primarily on an EV/EBITDA basis. This reflects the generally cash-generative nature of (asset light) construction, maintenance, repair, inspection, compliance, and lifecycle support activities, while also allowing for comparison across platforms with different end-market exposures, contract structures, and capital intensity.

Multiples are a mix of trailing and forward metrics, with the earnings period for each observed transaction stated in its description.

The analysis is primarily European-focused; however, we include select US comparables where relevant for valuation anchoring.

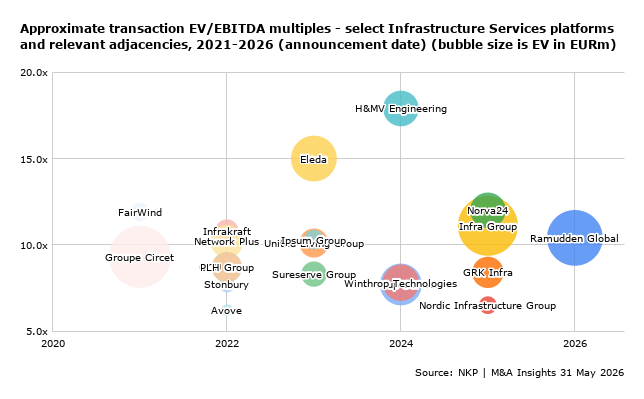

~10.4x

EV/adj. EBITDA (2025-12R)

Ramudden Global is an international provider of temporary traffic management and infrastructure safety services, supporting road, utility, construction, and broader infrastructure works. The business is relevant in an infrastructure-services valuation context as a scaled transport infrastructure safety platform, with demand linked to roadworks, network maintenance, public infrastructure upgrades, safety requirements, and the need to protect workers and road users around active infrastructure sites.

I Squared Capital, a global infrastructure investor, is set to acquire Ramudden Global at a reported valuation of approximately EUR 2.5bn. In FY25, the company reported revenue of approximately SEK 11,500m (EUR ~1,100m), and adjusted EBITDA of approximately SEK 2,500m (EUR ~240m). Based on the reported valuation and adjusted EBITDA, the transaction implies an EV/adj. EBITDA (FY0) of approximately 10.4x.

~6.5x

EV/adj. EBITDA (2025-12E)

Nordic Infrastructure Group, also known as Qben Rail, is a Norway-based rail infrastructure services provider focused on technical services across railway construction, maintenance, and related infrastructure works. The business is relevant in an infrastructure-services valuation context as a specialist rail platform exposed to long-term investment in transport infrastructure, recurring maintenance needs, and safety-critical public infrastructure assets.

In October 2025, Eleda Norge, part of Bain Capital- and Altor-backed Eleda Group, signed a final share purchase agreement to acquire 100% of Nordic Infrastructure Group from Qben Infra and ININ Group for a publicly disclosed total enterprise value of NOK 850m, including an earn-out of up to NOK 65m. Excluding the earn-out implies an enterprise value of approximately NOK 785m. According to Eleda Group’s 2025 annual report, the target generated revenue of NOK 1,260m in 2025. Based on an estimated adjusted EBITDA margin of approximately 9.5%, derived from the reported adjusted EBITA margin of 7.5% and an assumed depreciation-to-revenue ratio of approximately 2% (based on historic margins), adjusted EBITDA can be estimated at around NOK 120m. This implies an EV/adj. EBITDA (FY1) multiple of approximately 6.5x.

~11.1x

EV/EBITDA (2025-09E)

Infra Group is a European infrastructure services platform providing technical services across utility, energy, telecom, and broader infrastructure networks. The business is relevant in an infrastructure-services valuation context as a scaled platform operating in recurring, mission-critical service areas linked to the maintenance, upgrade, and lifecycle support of essential infrastructure assets, including utility, energy, telecom, and data centre-adjacent network infrastructure.

According to public reporting at the time, a consortium led by ICG agreed to acquire a partial stake in Infra Group from PAI Partners at a company valuation of approximately EUR 3.0bn. The group generated estimated pro forma revenue of approximately EUR 1,588m in 2025, including the effect of acquisitions completed during the first half of the year. Based on Infra Group’s historical EBITDA margin of approximately 17%, EBITDA can be estimated at around EUR 270m, implying an EV/EBITDA (FY0) multiple of approximately 11.1x. The transaction also implies an EV/Sales multiple of approximately 1.9x.

~12x

EV/EBITDA (2024-12R)

Norva24 Group is a Northern European underground infrastructure maintenance platform providing services including emptying, pressure flushing, pipe services, and related maintenance services for underground infrastructure networks. The business is relevant in an infrastructure-services valuation context as a scaled, recurring maintenance-led platform operating in essential wastewater, drainage, and underground network infrastructure, with demand supported by asset criticality, regulatory requirements, and the need for ongoing maintenance of ageing infrastructure.

Apax launched a recommended public cash offer of SEK 36.50 per share to acquire Norva24 Group, valuing the company’s equity at approximately SEK 6,630m. Adding net debt at the time of acquisition of approximately SEK 1,450m implies an enterprise value of approximately SEK 8,080m. Norva24 reported revenue of NOK 3,631m and EBITDA of NOK 676.2m for FY2024. Based on the implied enterprise value, the transaction corresponded to an EV/EBITDA (FY0) of approximately 12.0x.

~8.4x

EV/adj. EBITDA (2024-12R)

GRK Infra is a Finland-based infrastructure services group providing construction, maintenance, and technical services across transport, rail, environmental, and broader infrastructure markets. The business is relevant in an infrastructure-services valuation context as a scaled Nordic platform with exposure to essential infrastructure investment, lifecycle maintenance, and public-sector-driven demand.

At the time of its IPO on Nasdaq Helsinki, GRK Infra listed at a market capitalisation of approximately EUR 425m, implying an enterprise value of approximately EUR 513m, when including the firm’s EUR 88m net debt. For the financial year 2024, the company reported adjusted EBITDA of EUR 61.3m, reflecting an EV/adj. EBITDA (FY0) of approximately 8.4x.

~17.9x

EV/EBITDA (2024-12E)

H&MV Engineering is an Ireland-based specialist engineering services provider focused on high-voltage electrical infrastructure, grid connections, substations, and power-related technical services. The business is relevant in an infrastructure-services valuation context as a scaled, high-growth platform exposed to structurally attractive demand drivers across electrification, grid investment, renewable energy, data centre power demand, and high-voltage infrastructure supporting mission-critical facilities.

According to media reporting at the time, LGT Capital Partners made a minority investment in H&MV Engineering at an implied company valuation of approximately EUR 750m. Based on 2024 EBITDA of approximately EUR 42m expected at the time of acquisition, the transaction implied an EV/EBITDA (FY1E) of approximately 17.9x.

~7.7x

EV/adj. EBITDA (2024-03R)

M Group Services is a UK-based infrastructure services platform providing essential maintenance, repair, engineering, and support services across utilities, transport, telecom, energy, and broader infrastructure networks. The business is relevant in an infrastructure-services valuation context as a scaled platform with exposure to recurring, mission-critical workstreams linked to the maintenance, upgrade, and resilience of critical national infrastructure.

According to our analysis of Midas Midco Limited’s statutory accounts, CVC Capital Partners acquired M Group Services in June 2024 at an implied enterprise value of approximately GBP 993m. For the financial year ended March 2024, the business reported revenue of GBP 2,196m and EBITDA before exceptional and non-recurring items of GBP 129.7m, implying an EV/Sales (FY0) multiple of approximately 0.5x and an EV/adj. EBITDA (FY0) multiple of approximately 7.7x.

~7.8x

EV/EBITDA (2023-12R)

Winthrop Technologies is an Ireland-based data centre delivery and mission-critical infrastructure services provider, specialising in turnkey data centre construction and technical delivery across European markets. The business is relevant in an infrastructure-services valuation context as a scaled specialist platform serving AI, cloud, hyperscale, and enterprise data centre customers, with demand linked to rising compute requirements, power-intensive digital infrastructure, and the need for specialist execution capability in mission-critical environments.

According to reporting by The Times at the time, funds managed by Blackstone Tactical Opportunities and affiliated funds acquired a 50.7% stake in Winthrop Technologies, valuing the business at approximately EUR 800m. Winthrop reported 2023 revenue of approximately EUR 1.17bn and EBITDA of approximately EUR 103.2m, implying an EV/Sales of approximately 0.7x and an EV/EBITDA (FY0) of approximately 7.8x.

~15x

EV/EBITDA (2023-12E)

Eleda Group is a Sweden-based infrastructure services platform providing civil engineering, construction, maintenance, and technical services across transport, energy, water, and broader public infrastructure markets. The business is relevant in an infrastructure-services valuation context as a scaled Nordic platform with exposure to recurring infrastructure investment, public-sector demand, and long-term maintenance and upgrade needs across essential physical assets.

According to our analysis of Eleda TopCo AB’s statutory accounts, Bain Capital agreed to acquire Eleda Group from Altor at a valuation of approximately SEK 16.5bn (EUR 1.5bn). According to NKP | M&A Insights’ knowledge at the time, the business was marketed off revenue of approximately EUR 1,440m and EBITDA of approximately EUR 100m. This implies an EV/Sales multiple of approximately 1.0x and an EV/EBITDA (FY1E) of approximately 15.0x.

~8.3x

EV/EBITDA (2023-09R)

Sureserve Group is a UK-based provider of energy and compliance services primarily serving the social housing and public sectors. The business provides inspection, compliance, maintenance, installation, and energy-efficiency services across heating, electrical, fire, water, renewables, and broader regulated building-infrastructure systems. It is relevant in an infrastructure-services valuation context as a recurring, compliance-led technical services platform exposed to non-discretionary maintenance, public-sector-linked demand, and the decarbonisation and safety requirements of the UK housing stock.

Cap10 Partners acquired Sureserve Group in a public-to-private transaction completed on 11 July 2023, at an equity value of approximately GBP 214m, derived from the disclosed offer price of 125p per share. Based on reported net debt, including lease liabilities, of approximately GBP 4.3m in Sureserve’s H1-2023 report for the period ended March 2023, the transaction implied an enterprise value of approximately GBP 218.3m. For the financial year ended September 2023, Sureserve reported EBITDA of GBP 26.2m, reflecting an EV/EBITDA (FY1) multiple of approximately 8.3x, assuming Cap10 had reasonable visibility into the full-year result at the time of acquisition.

~10.1x

EV/adj. EBITDA (2023-03R)

United Living Group is a UK-based infrastructure, housing, and property services platform providing maintenance, regeneration, engineering, and infrastructure support services across regulated and public-sector-linked end-markets. The business is relevant in an infrastructure-services valuation context given its exposure to essential asset maintenance, utility infrastructure, housing infrastructure, and long-term customer relationships with public and regulated-sector clients.

According to our analysis of the statutory accounts of UL Intermediate I Limited, Apollo acquired United Living Group in May 2023 at an implied enterprise value of approximately GBP 404m. Based on adjusted EBITDA of approximately GBP 40m for the 2022/23 reporting period, the transaction implied an EV/adj. EBITDA (FY0) of approximately 10.1x.

~10.3x

EV/EBITDA (2022-12R)

Ipsum Group is a UK-based infrastructure services provider focused on maintenance, repair, inspection, and emergency response services across utility and infrastructure networks. The business is relevant in an infrastructure-services valuation context as a specialist platform serving essential network assets, with demand linked to asset reliability, regulatory requirements, planned maintenance, and the ongoing operation of critical infrastructure.

According to our analysis of Hydro Bidco Limited’s statutory accounts, IK Partners’ acquisition of Ipsum Group was carried out at an implied enterprise value of approximately GBP 82.7m. Based on reported 2022 revenue of GBP 81.5m and EBITDA of GBP 8.0m, the transaction implied an EV/Sales (FY0) of approximately 1.0x and an EV/EBITDA (FY0) of approximately 10.3x.

~7.7x

EV/EBITDA (2022-06R)

Stonbury is a UK-based specialist infrastructure services provider focused on the water and environmental infrastructure markets. The business provides inspection, maintenance, repair, refurbishment, and civil engineering services to water utilities and related regulated infrastructure customers. It is relevant in an infrastructure-services valuation context as a niche technical services platform exposed to recurring asset maintenance, regulatory-driven water infrastructure investment, and long-term framework relationships with essential-service providers.

According to our analysis of Project Sutton Bidco Limited’s statutory accounts, LDC’s acquisition of Stonbury in December 2022 was carried out at an implied enterprise value of approximately GBP 40m. For the financial year ended June 2022, the business reported EBITDA of around GBP 5.2m implying an EV/EBITDA (FY0) of approximately 7.7x.

10.8x

EV/EBITDA (2022-09 LTM)

Infrakraft is a Sweden-based infrastructure services provider focused on civil engineering, maintenance, and technical services for transport, rail, road, and broader public infrastructure assets. The business is relevant in an infrastructure-services valuation context as a Nordic platform exposed to recurring infrastructure maintenance, public-sector investment, and long-term demand for the upgrade and renewal of essential physical infrastructure.

According to our analysis of Infrakraft BidCo AB’s statutory accounts, Trill Impact’s September 2022 acquisition of Infrakraft was carried out at an implied enterprise value of approximately SEK 2,050m. At the time of acquisition, Infrakraft generated LTM revenue of approximately SEK 1.9bn, and its LTM EBITDA can be estimated at approximately SEK 190m based on a historic reported EBITDA margin of around 10% in 2021. This implies a pro forma EV/EBITDA (LTM) of approximately 10.8x.

~10.2x

EV/EBITDA (2022-06 LTM)

Network Plus is a UK-based infrastructure services provider delivering repair, maintenance, reinstatement, and technical field services across utility and energy networks. The business is relevant in an infrastructure-services valuation context as a scaled platform serving essential network infrastructure, with demand linked to recurring maintenance, asset reliability, emergency response, and long-term outsourcing by regulated utility customers.

According to our analysis of Nyetimber Finco Limited’s statutory accounts, OMERS Private Equity’s July 2022 acquisition of Network Plus was carried out at an implied enterprise value of approximately GBP 512m. The company was reportedly marketed off LTM EBITDA of approximately GBP 50m at the time, implying an EV/EBITDA of approximately 10.2x.

8.7x

EV/adj. EBITDA (2022-03R)

OCU Group is a UK-based infrastructure services provider delivering utility, energy, telecom, and water infrastructure services across regulated and essential network markets. The business is relevant in an infrastructure-services valuation context as a scaled technical services platform with exposure to recurring network maintenance, grid and utility upgrades, telecom infrastructure deployment, data centre-related power and connectivity demand, and long-term investment in critical national infrastructure.

According to our analysis of Oat Topco Limited’s statutory accounts, Triton’s July 2022 acquisition of OCU Group was carried out at an implied enterprise value of approximately GBP 395m. For the 2021/22 reporting period, the business reported adjusted EBITDA of approximately GBP 45.5m, implying an EV/adj. EBITDA (FY0) of approximately 8.7x.

~8.7x

EV/adj. EBITDA (2022-06 LTM)

PLH Group is a US-based utility infrastructure services platform providing construction, maintenance, repair, and technical field services across power delivery, communications, and gas utility networks. The business is relevant in an infrastructure-services valuation context as a scaled utility-focused platform serving essential network infrastructure, with demand linked to grid reliability, utility maintenance, emergency response, communications infrastructure investment, and long-term outsourcing by regulated utility customers.

According to public reports at the time, Primoris Services acquired PLH Group in June 2022 for an enterprise value of approximately USD 470m. At the time of the transaction, PLH Group generated LTM adjusted EBITDA of approximately USD 54m, implying an EV/adj. EBITDA (LTM) of approximately 8.7x.

~6.2x

EV/EBITDA (2022-12R)

Avove is a UK-based infrastructure services provider focused on water, wastewater, and broader utility infrastructure markets. The business provides design, maintenance, repair, upgrade, and delivery services for regulated infrastructure customers, making it relevant in an infrastructure-services valuation context as a technical services platform exposed to essential network maintenance, regulatory investment cycles, and long-term water infrastructure spending.

According to our analysis of Ersa Topco Limited’s statutory accounts, Rubicon Partners’ April 2022 acquisition of Avove was carried out at an implied enterprise value of approximately GBP 20.4m. Based on EBITDA for the 2022 reporting period, the transaction implied an EV/EBITDA (FY1) of approximately 6.2x.

~11.9x

EV/EBITDA (2020-12R)

FairWind is a Denmark-based wind turbine installation and servicing platform providing technical services across onshore and offshore wind infrastructure. The business is relevant in an infrastructure-services valuation context as a specialist renewable energy services provider exposed to wind power installation, maintenance, lifecycle support, and the broader energy transition.

According to our post-acquisition analysis of Force Holdco A/S, Triton’s September 2021 acquisition of FairWind was carried out at an estimated enterprise value of approximately DKK 595m. FairWind reported 2020 EBITDA of DKK 50.2m, implying an entry EV/EBITDA (FY0) multiple of approximately 11.9x.

~9.3x

EV/EBITDA (2021-03 LTM)

Groupe Circet is a France-based telecom infrastructure services platform providing engineering, deployment, operation, maintenance, and upgrade services across fixed and mobile communications networks. The business is relevant in an infrastructure-services valuation context as a scaled network services platform exposed to fibre rollout, mobile network investment, telecom outsourcing, and the lifecycle management of critical digital infrastructure.

In May 2021, Intermediate Capital Group acquired Groupe Circet from Advent International at an implied enterprise value of approximately EUR 3.2-3.3bn according to sources at the time. Based on the company’s pro forma LTM EBITDA of around EUR 350m reported by media at the time, the transaction corresponded to an EV/EBITDA (LTM) multiple of 9.1x-9.5x.

Across the analysed transactions, EV/EBITDA outcomes for Infrastructure Services platforms range from approximately 6x to the high-teens, with most observed transactions clustering around 8x–12x.

However, the range is broad because Infrastructure Services is not a homogeneous valuation category. Multiples vary materially depending on recurring maintenance exposure, contract quality, end-market resilience, technical differentiation, margin profile, delivery risk, and whether the business is primarily a local service provider, a scaled network services platform, or a specialist platform exposed to structural investment themes such as electrification, grid expansion, data centre capacity growth, and mission-critical infrastructure.

Broadly:

The key takeaway is that Infrastructure Services are not valued simply as “infrastructure exposure.” The market appears to pay most consistently for businesses that convert infrastructure demand into visible earnings, defensible customer relationships, technical capability, strong delivery infrastructure, and the ability to scale across geographies or service lines. In practice, valuation premiums are more likely where a platform is linked to structural investment themes such as electrification, grid expansion, data centre power demand, mission-critical infrastructure, telecom infrastructure, water and wastewater renewal, rail investment, infrastructure safety, renewable energy, or energy transition. By contrast, more labour-intensive, project-led, or locally dependent service providers may remain attractive but typically trade closer to core mid-market services multiples unless they demonstrate clear consolidation potential, specialist capabilities, or differentiated customer access.

Valuation dispersion in Infrastructure Services is driven less by the broad infrastructure label itself and more by differences in revenue visibility, contract quality, technical complexity, end-market exposure, and scalability. In practice, buyers are underwriting how repeatable, defensible, and expandable the earnings base is, rather than simply paying for exposure to infrastructure investment.

Key drivers typically include:

1. Recurring maintenance and lifecycle exposure

Platforms with revenue tied to recurring maintenance, repair, inspection, compliance, emergency response, and long-term asset lifecycle support tend to attract stronger buyer interest than businesses primarily dependent on one-off projects. The more closely a provider is embedded in keeping essential assets operational, safe, and compliant, the more durable the revenue profile is perceived to be.

2. Contract quality and customer embeddedness

Framework agreements, multi-year contracts, regulated customer relationships, and long-standing public-sector or utility relationships can materially improve revenue visibility. Buyers typically value businesses more highly where customer relationships are supported by asset knowledge, technical qualifications, local delivery capability, safety standards, and switching friction.

3. End-market exposure and structural growth

Not all infrastructure exposure is valued equally. Platforms linked to grid investment, electrification, data centre infrastructure, renewable energy, water and wastewater renewal, telecom networks, rail upgrades, infrastructure safety, and energy efficiency often benefit from stronger structural growth narratives. Data centre exposure is increasingly relevant, as AI-driven compute demand is accelerating the need for high-voltage connections, substations, grid reinforcement, backup power infrastructure, fibre connectivity, and specialist technical services around mission-critical facilities. Businesses serving slower-growing or more discretionary project markets may trade at lower levels, even where they operate within infrastructure.

4. Technical specialisation and regulatory relevance

Services that require accreditation, specialist engineering capabilities, safety-critical execution, or regulatory compliance tend to be more defensible than commoditised civil works or general contracting. Higher technical barriers can support pricing power, customer retention, and a more differentiated market position.

5. Margin quality and delivery risk

Infrastructure services platforms can vary significantly in profitability depending on labour intensity, project risk, subcontractor exposure, cost inflation, and contract structure. Buyers generally pay more for businesses with stable margins, disciplined project selection, limited fixed-price delivery risk, and a proven ability to manage operational execution across multiple sites or regions.

6. Platform scalability and buy-and-build potential

Fragmentation creates opportunity, but valuation premiums are more likely where the company can act as a true consolidation platform. This requires management depth, standardised processes, central functions, integration capability, a proven buy-and-build capability, and the ability to expand across geographies, customers, or adjacent service lines without materially increasing execution risk.

In practice, valuation outcomes depend less on whether a company serves infrastructure end-markets and more on the specific sub-segment of the end market and the quality of the earnings model behind that exposure: how recurring the work is, how embedded the customer relationships are, how differentiated the technical capabilities are, and how convincingly the platform can scale, combined with end-market demand growth.

The buyer universe in Infrastructure Services includes private equity sponsors, infrastructure-oriented investors, listed industrial groups, technical services consolidators, and strategic buyers active across data centres, utilities, energy, telecom, transport, water, rail, road, and public infrastructure markets.

Buyer appetite is supported by the sector’s exposure to essential assets and long-term infrastructure renewal. Many targets operate close to the physical asset base, providing maintenance, repair, inspection, installation, compliance, emergency response, and lifecycle support services that are required to keep networks and public assets safe, operational, and compliant.

Sponsor-to-sponsor transactions and public-to-private activity suggest that scaled Infrastructure Services platforms remain attractive once they have established customer trust, operational discipline, and a credible consolidation runway. Competition is typically strongest for assets that combine essential infrastructure exposure with repeatable work, technical barriers, and the ability to scale without taking on excessive single-project risk.

M&A activity in European Infrastructure Services has increased as the sector sits at the intersection of several long-duration investment cycles. Electrification, an explosive growth for data centres driven by AI, grid reinforcement, telecom network upgrades, water and wastewater renewal, rail modernisation, road safety, energy efficiency, and broader public infrastructure spending are all creating demand for specialist delivery capacity.

Unlike sectors where demand is mainly linked to discretionary corporate spending, Infrastructure Services is often tied to physical asset condition, regulatory obligations, safety requirements, and network uptime. This gives the sector a degree of resilience, but also creates operational bottlenecks: customers increasingly need partners with enough technicians, equipment, permits, accreditations, local density, and project management capability to deliver work reliably across regions.

This has made scale more strategically important. Larger platforms are better positioned to win framework agreements, absorb labour and equipment constraints, invest in systems, manage compliance requirements, and serve customers across multiple geographies or infrastructure verticals. At the same time, many local and specialist providers remain sub-scale, creating opportunities for consolidation.

Recent transactions across utility services, telecom infrastructure, rail, water, road safety, underground infrastructure maintenance, and technical building services suggest that buyer appetite is not limited to one infrastructure vertical. Instead, investors are targeting businesses that can convert long-term infrastructure spending into repeatable earnings through customer embeddedness, delivery capability, and operational discipline.

Subscriber edition

[EXCLUSIVE TO SUBSCRIBER EDITION]

by revenue, service segment, and ownership type (bubble size = EBITDA)

Revenue and EBITDA figures are approximate and partly from non-public sources. The figures predominantly relate to the most recent reporting period available, typically 2024 or 2025, with selected 2026 estimates included where relevant.

[EXCLUSIVE TO SUBSCRIBER EDITION]

Infrastructure Service segments as shown in the bubble chart:

[EXCLUSIVE TO SUBSCRIBER EDITION]

Subscriber edition

The following section highlights a selection of emerging M&A situations currently monitored by NKP | M&A Insights across the European Infrastructure Services landscape.

The situations span utility services, telecom infrastructure, transport infrastructure, water and underground infrastructure, data centre infrastructure services, technical building infrastructure, and broader asset lifecycle support. Some remain pre-process or early-stage, while others are understood to be more advanced, with advisor involvement, buyer outreach, or formal process preparation already underway.

Company identities and selected transaction details have been intentionally blinded. The purpose of this section is not to disclose specific processes, but to provide forward-looking situational awareness around where infrastructure services consolidation is forming and which parts of the market appear most active.

Based on the situations currently tracked, the emerging opportunity set is not concentrated in a single infrastructure vertical. Instead, activity is forming across several pockets where long-term infrastructure investment, AI-driven data centre demand, electrification, technical labour constraints, recurring maintenance needs, and fragmented local supply are creating demand for larger and more institutionalised service platforms.

To retrieve additional context, including the names of the referenced companies - search for relevant terms such as “infrastructure services”, “utility services”, or “telecom infrastructure” (including the quotation marks) in the search field in Companies for Sale or contact us at research@mainsights.io for assistance.

Based on emerging situations currently being monitored across European Infrastructure Services, several themes appear to be shaping the next phase of consolidation.

Infrastructure owners increasingly need service providers that can deliver across regions, asset classes, and technical disciplines. Labour availability, equipment utilisation, framework requirements, safety standards, and project-management complexity all favour larger platforms with established operating infrastructure. This is likely to support continued consolidation among regional specialists that lack the scale to serve larger customers efficiently.

The rapid growth of AI workloads is accelerating demand for new data centre capacity and placing pressure on power availability, grid connections, cooling infrastructure, backup power, fibre connectivity, and high-specification technical installation. This is creating demand for specialist infrastructure services providers capable of delivering construction support, electrical infrastructure, high-voltage works, mechanical and cooling systems, commissioning support, maintenance, and lifecycle services for data centre environments. Platforms with credible exposure to data centre infrastructure are likely to attract strong buyer interest where they combine technical capability, delivery capacity, customer access, and exposure to recurring expansion or maintenance work.

Grid reinforcement, high-voltage connections, renewable power integration, EV infrastructure, data centre power demand, and broader electrification needs are creating demand for specialist engineering and field-service capacity. Platforms with proven technical capability in power infrastructure, grid services, and energy-related maintenance are likely to remain highly attractive to both sponsors and strategic buyers.

Aging water, wastewater, road, rail, telecom, and utility networks are increasing the need for repair, renewal, upgrade works, asset replacement, and emergency response services. This supports demand for businesses that are embedded in ongoing asset upkeep rather than dependent only on new-build projects. Acquirers are likely to focus on platforms that can demonstrate recurring or framework-based revenue, high customer retention, and exposure to non-discretionary maintenance cycles.

Many infrastructure services markets remain highly dependent on skilled technicians, permits, safety procedures, equipment availability, project management, and local delivery capability. As customer requirements become more demanding, smaller operators may face increasing pressure around recruitment, training, systems, compliance, and working capital. This could create both acquisition supply and a stronger competitive position for scaled platforms.

The sector benefits from structural demand, but not all infrastructure exposure will be valued equally. Premium interest is likely to centre on businesses with clear earnings visibility, disciplined project risk, technical differentiation, and credible scalability. More project-led, low-margin, or locally concentrated businesses may still transact, but are likely to be viewed mainly as bolt-ons unless they bring scarce capabilities, customer access, or strategic geographic density.

The situations below represent a selection of emerging opportunities currently monitored within the Northern European Infrastructure Services landscape. These situations vary in maturity, ranging from early-stage strategic discussions to situations where more formal processes may emerge over time - company names and identifying details have been intentionally omitted.

[EXCLUSIVE TO SUBSCRIBER EDITION]

Taken together, the emerging situations currently tracked across Infrastructure Services point to a market where demand remains structurally supported, but where buyer focus is increasingly selective.

First, the sector benefits from several long-duration investment themes. Grid reinforcement, electrification, telecom rollout, water and wastewater renewal, rail upgrades, road infrastructure, energy efficiency, and renewable energy services are all creating sustained demand for specialist delivery capacity. This supports continued interest in platforms that sit close to essential assets and provide services required to keep infrastructure operational, safe, and compliant.

Second, scale is becoming more important as customers require broader geographic coverage, stronger technical capabilities, better systems, and reliable execution across complex work programmes. This favours platforms with established management teams, framework positions, technician capacity, equipment infrastructure, and the ability to manage safety, compliance, labour utilisation, and project risk across multiple regions.

Third, the opportunity landscape differs by sub-segment. Utility, energy, telecom, water, and underground infrastructure services appear particularly well positioned given the combination of regulatory pressure, ageing assets, and long-term network investment. Technical building infrastructure and renewable energy services also remain attractive, but buyers are likely to scrutinise customer mix, contract quality, margin stability, and exposure to project-based delivery more closely.

Valuation expectations should therefore be anchored in the quality and repeatability of earnings, not infrastructure exposure alone. Premium outcomes are most likely for businesses with recurring or framework-based revenue, strong customer embeddedness, technical differentiation, disciplined project execution, and a credible ability to scale. More locally concentrated or project-led operators may remain attractive as bolt-ons, but are less likely to command platform-level valuations unless they bring scarce capabilities, strategic customer access, or meaningful regional density.

Overall, Infrastructure Services consolidation is likely to remain active, but competition should be strongest for assets that combine essential infrastructure exposure with visible earnings, operational maturity, and a clear role in the ongoing renewal, maintenance, and upgrade of critical networks and public assets.

Valuation references in this analysis are indicative and reflect NKP | M&A Insights’ assessment of historical transactions based on publicly available information at the time of writing, including statutory accounts, regulatory filings, credit rating agency reports, sponsor materials and company press releases.

Where enterprise values are not explicitly disclosed, they are derived from disclosed consideration, debt assumptions, or implied values in transaction vehicles (e.g. BidCo / TopCo entities), cross-checked against available filings.

EBITDA figures reflect the metric referenced at the time of marketing where identifiable (e.g. adjusted EBITDA), or NKP’s assessment based on the most recent published annual accounts.

For clarity:

Where forward EBITDA was used in marketing materials, multiples are presented on an FY1 basis. Where historical accounts were the primary reference, multiples are presented on an FY0 basis. The basis applied is specified in each transaction summary.

In certain cases, EBITDA may reflect normalisation adjustments or full-year effects of completed acquisitions where such information was clearly disclosed. These adjustments reflect NKP’s assessment and may differ from buyer-underwritten figures.

Where precise figures are unavailable, ranges or approximations are used based on best available sources. All valuation references should therefore be interpreted as directional indicators rather than definitive transaction terms.

Supporting detail and transaction backup materials are available to NKP subscribers.

This report has been prepared by NKP | M&A Insights for informational purposes only. While NKP | M&A Insights has taken reasonable care to ensure that the information contained herein is accurate and based on reliable sources at the time of publication, no representation or warranty, express or implied, is made as to the accuracy, completeness, or timeliness of the information.

The analysis, views and conclusions expressed in this report reflect NKP | M&A Insights’ interpretation of publicly available information and proprietary intelligence sources and may be subject to change without notice.

Nothing in this report constitutes investment advice, an offer to sell, or a solicitation to buy any securities or assets. NKP | M&A Insights shall not be held liable for any direct or indirect loss arising from the use of, or reliance on, the information contained in this report.

This report is intended solely for the use of NKP subscribers and may not be reproduced, redistributed, or circulated without prior written consent from NKP | M&A Insights.

Download as PDF

Download as PDFWhether you are exploring a subscription or would like to discuss a situation relevant to our coverage, you are welcome to contact us directly.