A report by NKP | M&A Insights - Subscriber Edition

Mapping valuation dynamics and emerging opportunities across Accounting Services platforms

Updated: 4 May 2026

This subscriber edition maps valuation outcomes and consolidation dynamics across primarily Northern European Accounting Services Platforms - and highlights where M&A activity is currently forming.

Based on a set of observed transactions (2018–2025) and NKP | M&A Insights’ proprietary tracking of emerging situations, we show why Accounting Services is not a single valuation category and what structurally drives dispersion across sub-segments.

The analysis is intended to support investors and advisors in understanding both current valuation benchmarks and the forward pipeline of potential opportunities as currently observed (as of 4 May 2026).

NKP | M&A Insights provides proprietary, validated, early-stage M&A intelligence across Northern Europe - surfacing and contextualising non-public ownership and transaction dynamics, often months before formal processes emerge and broader market visibility.

Subscribers receive a daily curated intelligence feed, continuous tracking of emerging and live situations, and embedded cross-border context on combination opportunities, valuation levels, and buyer mappings. On average, we surface 5–7 new situations daily, most of which are not covered by traditional M&A platforms, and typically months before broader market visibility.

Trusted by 200+ private equity and advisory teams, NKP acts as an intelligence infrastructure layer to reduce information asymmetry and strengthen origination and competitive positioning.

The situations referenced in this report draw on this intelligence base and are intended to provide additional forward-looking context alongside the valuation analysis presented herein.

Table of Contents

Context and definitions 4

Defining Accounting Services platforms 4

Why Accounting Services platforms attract buyer interest 4

Market structure and sub-segmentation 5

Historical transaction outcomes 6

Observed valuation range in Accounting Services platforms 15

What actually drives valuation dispersion in Accounting Services platforms 17

Buyer Landscape in Accounting Services Platforms 18

Private equity interest is typically driven by: 18

Strategic buyers focus on: 19

Increasing M&A activity in European Accounting Platforms 19

Key drivers 19

Ownership landscape of 39 selected Accounting Services platforms [SUBSCRIBER EDITION ONLY] 20

Emerging and current opportunities landscape [SUBSCRIBER EDITION ONLY] 23

Forward-looking market observations 23

Emerging situations currently tracked by NKP | M&A Insights 24

Implications for investors and strategic buyers 24

Appendix 25

Methodology note 25

Disclaimer 26

For the purpose of this analysis, Accounting Services platforms refer to businesses that provide recurring financial administration, reporting, compliance, and related advisory services embedded in clients’ ongoing finance and regulatory workflows.

These platforms typically sit within core back-office and finance functions such as bookkeeping, accounts preparation, tax compliance, payroll, financial reporting, and selected assurance or advisory services delivered as part of an ongoing client mandate.

This includes providers offering:

The defining characteristic across these platforms is that services are embedded in recurring, operationally critical, and often compliance-driven client workflows, rather than delivered as one-off advisory or project-based engagements.

This analysis does not include:

Accounting Services platforms have attracted sustained buyer interest due to a combination of recurring compliance obligations, embedded client relationships, fragmented market structures, and resilient demand characteristics.

Across SMEs, mid-market companies, and larger enterprises, accounting, tax, payroll, audit, and related finance processes remain non-discretionary. The operational burden, regulatory importance, and trust required to deliver these services often support long-term outsourcing to specialist providers.

From a buyer and investor perspective, this typically translates into:

In addition, many accounting services platforms have expanded from traditional bookkeeping or compliance mandates into broader advisory, outsourced finance, payroll, and technology-enabled service models, creating opportunities for cross-sell, operational leverage, and platform expansion post-acquisition.

As a result, well-positioned Accounting Services platforms often exhibit revenue durability and cash generation characteristics that continue to attract both financial sponsors and strategic consolidators.

While often grouped under a single “accounting services” label, the sector spans multiple sub-segments with materially different operating models and valuation characteristics. The key dividing lines are not simply between bookkeeping, tax, payroll, and audit, but between local compliance delivery, broader multidisciplinary client-account platforms, and technology-enabled operators capable of scaling more efficiently.

At one end of the spectrum are traditional SME-focused accounting, bookkeeping, payroll, and tax compliance firms. These businesses benefit from recurring, non-discretionary demand, but are often labour-intensive, locally anchored, and constrained by practitioner capacity, succession issues, and price pressure in more standardised work.

A second group consists of broader accountancy platforms combining compliance-led services with audit, assurance, tax, and advisory. These businesses typically benefit from stronger client ownership and broader wallet share, but also operate within more complex regulatory and governance frameworks, particularly where audit is material.

Finally, technology-enabled accounting consolidators increasingly form a distinct category, where automation, centralised infrastructure, and buy-and-build execution support greater scalability and, in many cases, higher valuation outcomes.

Understanding where a company sits within this spectrum is critical to interpreting valuation outcomes.

Transaction details, valuation metrics, and supporting context are available to NKP subscribers.

Given the mix of large-scale consolidation platforms and smaller, owner-managed accounting practices, valuation references are presented primarily on an EV/EBITDA basis, reflecting the predominantly cash-generative and margin-stable character of accounting services businesses; EV/Sales is additionally referenced where EBITDA was unavailable.

Multiples are a mix of trailing and forward metrics, with the earnings period for each observed transaction stated in its description.

The analysis is primarily European-focused; however, we include select US comparables where relevant for valuation anchoring.

~1.6x

EV/Sales (2025-05R)

Wipfli is a US-based advisory and accounting firm providing audit, tax, and broader professional services primarily to middle-market clients. The business operates across a wide range of accounting and advisory disciplines and maintains the type of recurring, deeply embedded client relationships characteristic of scaled professional services platforms. It is relevant in an accounting-services valuation context as a sizable platform with meaningful advisory exposure.

According to public reporting at the time, New Mountain Capital agreed to acquire a significant minority stake of approximately 40% in Wipfli at an enterprise value of above USD 1 billion. For the financial year ended 31 May 2025, Wipfli reported net revenue of USD 612m, implying an EV/Sales (FY0) of approximately 1.6x. No EV/EBITDA multiple has been presented, as the target did not publish audited financial statements.

6.2x

EV/EBITDA (2024-12R)

Baker Tilly South East Europe’s operations constitute a professional services business providing audit, tax, advisory, legal, and corporate services across Cyprus, Greece and the wider South-East Europe region. The business is relevant in an accounting-services valuation context as a cross-border SME and mid-market accountancy platform acquired by a listed UK accountancy consolidator in the context of active European geographic expansion, illustrating the valuation dynamics associated with smaller, regionally embedded professional services businesses.

According to the transaction terms announced at the time, MHA agreed to acquire Baker Tilly's Greece and Cyprus unit for EUR 24m. The business reported 2024 revenue of EUR 19.4m and adjusted EBITDA of EUR 3.9m, reflecting an EV/Sales (FY0) of 1.2x and an EV/EBITDA (FY0) of 6.2x.

~2.3x

EV/Sales (2024-12R)

Moss Adams is a large US-based certified public accounting and advisory firm with deep industry specialisation and a well-established footprint across the Western United States, providing audit, tax, and advisory services to a broad middle-market and institutional client base. The transaction is relevant in an accounting-services valuation context as an illustration of the valuations being ascribed to large-scale CPA consolidation platforms.

According to Reuters, Baker Tilly US announced in April 2025 a definitive agreement to merge with Moss Adams in a transaction valued at approximately USD 7 billion, creating the sixth-largest CPA and advisory firm in the United States, backed by additional investment from Hellman & Friedman and Valeas Capital Partners. The transaction valued the combined entity at approximately USD 7 billion; Baker Tilly US and Moss Adams generated combined annual revenue of approximately USD 3.1 billion in FY2024 (USD 1.8 billion and USD 1.3 billion, respectively), implying an EV/Sales multiple of approximately 2.3x. Moss Adams operated as a private LLP and did not publish audited financial statements; accordingly, no EV/EBITDA multiple has been presented.

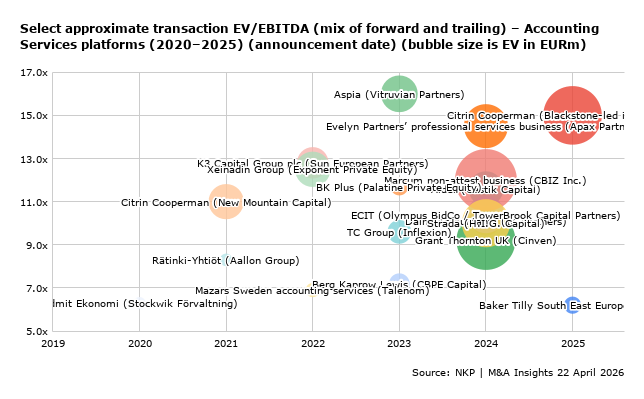

15.0x

EV/EBITDA (2024-12R)

Citrin Cooperman is a leading US-based professional services firm providing tax, advisory, and accounting services primarily to private middle-market businesses and high-net-worth individuals. The business is relevant in an accounting-services valuation context as a top-20 US accounting firm and as the first PE-to-PE ownership transition of a CPA firm at this scale, both of which illustrate sustained institutional appetite for large, recurring-revenue accounting platforms.

According to established financial media (Financial Times and the Wall Street Journal), Blackstone led a consortium acquiring a majority stake of over two-thirds in Citrin Cooperman from New Mountain Capital at an enterprise value of over USD 2.0bn. Based on the same reporting, the transaction implied an EV/EBITDA multiple of approximately 15.0x (FY0), corresponding to implied EBITDA of c. USD 133m, up from the c. 11.0x multiple at which New Mountain originally acquired its stake in October 2021. The same sources indicate that Citrin Cooperman generated approximately USD 850–900m of revenue in 2024, implying an EV/Sales multiple of approximately 2.2–2.4x (FY0).

~10.1x

EV/EBITDA (2025-03R)

Dains Accountants is a UK-based provider of accountancy and business advisory services to SMEs, established in 1926 and serving over 17,000 clients through approximately 765 employees at the time of the transaction. The business had been scaled through 10 acquisitions and sustained organic growth since Horizon Capital's 2021 investment, and is relevant in an accounting-services valuation context as a mid-market UK accountancy consolidation platform undergoing a second-generation private equity ownership transition, with IK Partners succeeding as the majority shareholder to support the next phase of buy-and-build expansion.

According to our analysis of Pebble Topco Limited's (the acquisition vehicle's) statutory accounts, IK Partners acquired a majority stake in Dains at an implied enterprise value of GBP 202m. The business had pro forma adjusted EBITDA above GBP 20m for the financial year ended March 2025 (2024/25R ~ FY1), the transaction thus reflecting an EV/EBITDA (FY1) of approximately 10.1x.

~9.2x

EV/EBITDA (2024-12R)

Grant Thornton UK is one of the leading diversified professional services firms in the United Kingdom, providing audit, tax, and advisory services across a broad range of sectors and client segments. The business is relevant in an accounting services valuation context as a large-scale, top-tier, branded accountancy platform and as one of the most significant private equity investments in the UK professional services sector in recent years.

According to the Financial Times, Cinven made a majority strategic investment in Grant Thornton UK at an enterprise value of up to GBP 1.5 billion. Per the firm's audited statutory accounts filed at Companies House, Grant Thornton UK reported net revenue of GBP 724.0 million and EBITDA of GBP 163.9 million for the financial year ended 31 December 2024, reflecting an EV/Sales and EV/EBITDA (FY1) of up to 2.1x and 9.2x, respectively.

14.5x

EV/EBITDA (2024-09R)

Evelyn Partners’ professional services business, also known as Smith & Williamson accountants, is a UK-based accounting, tax, and advisory platform, carved out from the broader Evelyn Partners group. The business is relevant in an accounting-services valuation context as a sizeable standalone UK accountancy and advisory platform and as an example of valuations achievable in carve-out transactions.

According to Financial News, Apax Partners agreed to acquire Evelyn Partners' professional services business for GBP 700 million, reflecting an EV/EBITDA (FY0) of 14.5x on an implied EBITDA of approximately GBP 48 million.

11.6x

EV/EBITDA (2024-12E)

Aider is a Norwegian tech-enabled accounting and consulting services firm providing accounting, advisory, and digital services primarily to SMEs, having grown rapidly through a buy-and-build programme of approximately 50 acquisitions since its founding in 2019, reaching approximately 1,100 employees at the time of the transaction. The business is relevant in an accounting-services valuation context as a scaled Nordic accounting consolidation platform, illustrating how high-growth, technology-enabled operators with proven buy-and-build execution can transact toward the upper end of the core platform range.

According to our analysis of Aider Group AS's 2024 statutory accounts, the investment by Castik Capital in October 2024 was carried out at an enterprise value of NOK 2.9 billion. According to NKP's sources at the time, Aider was marketed off an EBITDA of NOK 250m, implying an EV/EBITDA (2024E ~ FY1) of 11.6x. Expected 2024 revenues were approximately NOK 1,500m, implying an EV/Sales (FY1) of 1.9x.

10.4x

EV/EBITDA (H1-2024/LTM)

ECIT is a Norwegian provider of accounting, IT services, and business advisory solutions, serving SMEs and mid-market clients across the Nordic region through an integrated platform that combines accounting services with IT- and technology-enabled workflows. The business is relevant to the valuation of accounting services, as its hybrid model spans both professional accounting services and IT solutions.

According to ECIT's company announcement of 1 August 2024, Olympus BidCo made a voluntary offer at NOK 10 per share, corresponding to an equity value of approximately NOK 4,650 million. Adding reported net debt of NOK 827 million as of H1-2024 (IFRS 16-consistent) implies an enterprise value of approximately NOK 5,477 million. Per ECIT's published H1-2024 financials, the business reported LTM revenue of NOK 3,752 million and LTM EBITDA of NOK 525 million, reflecting an EV/Sales of approximately 1.5x and an EV/EBITDA of approximately 10.4x.

12.0x

EV/EBITDA (2023-12R)

Marcum LLP is a leading US-based certified public accounting and advisory firm providing audit, tax, and business advisory services, with particular strength in serving private middle-market businesses, financial services clients, and high-growth companies. The transaction is relevant in an accounting-services valuation context as a large-scale CPA platform combination that created one of the largest accounting firms in the United States.

According to CBIZ's investor presentation filed with the SEC, the transaction valued Marcum's non-attest business at an enterprise value of approximately USD 2.3 billion, reflecting an EV/EBITDA (FY0) of approximately 12.0x on FY 2023 adjusted EBITDA.

~10x

EV/EBITDA (2023-12E)

Strada, comprising Alight's Professional Services segment and Payroll & HCM Outsourcing businesses, is a US-based provider of payroll processing, human capital management outsourcing, and professional services. The business is relevant as a reference point for payroll and compliance-adjacent professional services platforms, where recurring, deeply embedded process workflows drive valuation dynamics broadly comparable to those in accounting services.

According to Alight's official announcement, Alight agreed to sell Strada to an affiliate of H.I.G. Capital for up to USD 1.2 billion, comprising USD 1 billion in upfront cash consideration and up to USD 200 million in seller notes, with USD 150 million of the latter contingent on 2025 financial performance. This reflected an EV/adj. EBITDA (2023-12E ~ FY0) of approximately 10.0x and EV/Sales (2023-12E ~ FY0) of approximately 1.2x.

16.0x

EV/EBITDA (2023-12R)

Aspia is a Swedish provider of technology-enabled accounting, payroll, tax, and advisory services to SMEs, formed in 2018 through IK Partners' acquisitions of PwC Sweden's and KPMG Sweden's respective accounting divisions alongside Skeppsbron Skatt, and subsequently scaled into a leading Nordic accounting services platform through active digitalisation and operational integration under IK's ownership. The business is relevant in an accounting services valuation context as a scaled, tech-enabled accounting consolidation platform, providing a meaningful benchmark for valuations achievable at the upper end of the Nordic accounting services market following a sustained period of investment and margin improvement.

According to the official press release at the time, IK Partners agreed to sell Aspia to Vitruvian Partners, though the financial details of the transaction were not disclosed. The implied enterprise value of approximately SEK 5,200m has been derived through NKP's analysis of the statutory accounts of the holding entity UBC Ledgers Holding AB. For the financial year 2023, Aspia reported revenue of SEK 1,674m and EBITDA of SEK 325m, the transaction thus reflecting an EV/Sales (FY1) of 3.1x and an EV/EBITDA (FY1) of 16.0x.

~11.7x

EV/EBITDA (2023/24-03R)

BK Plus is a Midlands-headquartered UK accountancy firm founded in 2021, providing accounting and advisory services to SMEs through an active buy-and-build strategy, having assembled a network of over ten offices and approximately 300 staff by the time of the transaction. The business is relevant in an accounting-services valuation context as an early-stage UK accountancy consolidation platform.

According to our analysis of Project Crown Topco Limited’s statutory accounts, Palatine Private Equity invested in BK Plus at an implied enterprise value of GBP 24.6m. Based on the reported FY2023/24-03 revenue of c. GBP 14.0m and EBITDA before exceptional items of c. GBP 2.1m, this implied EV/Sales and EV/EBITDA (FY1) of approximately 1.8x and 11.7x, respectively.

9.6x

EV/EBITDA (2022-12R)

TC Group is a UK-based provider of accountancy, taxation, and professional services to SMEs, offering a broad range of compliance-driven accounting and advisory services to owner-managed businesses and mid-market clients. The business is relevant in an accounting-services valuation context as a regional UK accountancy platform acquired by an established mid-market private equity firm, illustrating the valuations achievable for well-run, organically growing SME-focused accountancy businesses with recurring client relationships.

According to our analysis of Auctus Topco Limited's (the acquisition vehicle's) statutory accounts, Inflexion acquired a majority stake in TC Group at an implied enterprise value of GBP 97m. TC Group reported adjusted EBITDA of GBP 10.1m for the financial year 2022, reflecting an EV/EBITDA (FY0) of 9.6x.

7.2x

EV/EBITDA (2022/23-03R)

Berg Kaprow Lewis (BKL) is a UK-based accountancy firm specialising in property, financial services, and tax, providing accounting, audit, and advisory services to over 5,000 clients through a team of more than 200 professionals. The business is relevant in an accounting services valuation context as a specialist mid-market UK accountancy platform, supported by a private equity investor, pursuing technology investments and strategic acquisitions.

According to our analysis of Bridge Topco UK Limited's (the acquisition vehicle's) statutory accounts, CBPE Capital invested in BKL at an implied enterprise value of GBP 52m, implying an EV/EBITDA (FY0) of 7.2x and an EV/Sales (FY0) of 2.6x, based on revenue of c. GBP 19.7m and EBITDA of c. GBP 7.2m.

12.8x

EV/EBITDA (2021/22-05R)

K3 Capital Group is a UK-based multi-disciplinary professional services group providing M&A advisory, tax advisory, and restructuring services primarily to SME clients. While not a provider of traditional accounting or audit services, the group's tax and restructuring operations serve an adjacent SME client base and provide a broader reference point for professional services valuations.

According to our analysis of Shin Topco Limited's (the acquisition vehicle's) statutory accounts, Sun European Partners acquired K3 Capital Group at an implied enterprise value of approximately GBP 261m, reflecting an EV/EBITDA (2021/22-05R ~ FY0) of 12.8x based on adjusted EBITDA of approximately GBP 20.4m.

6.9x

EV/EBITDA (2021-12E)

Mazars Sweden's accounting services division is a Swedish accountancy business providing accounting and bookkeeping services to SMEs in the Stockholm, Skåne and Gothenburg regions, with 46 FTEs at the time of the transaction. The business is relevant in an accounting services valuation context as a small-scale Nordic carve-out, illustrating the lower end of the valuation range for accounting services businesses acquired by strategic consolidators.

According to the transaction announcement at the time, Talenom – the Finnish publicly listed accounting firm – agreed to acquire Mazars Sweden's accounting services division for SEK 76m (incl. earnouts). For the financial year 2021, the division reported revenues of SEK 55m and estimated EBITDA of SEK 11m; the transaction thus reflecting an EV/Sales (FY0) of 1.4x and an EV/EBITDA (FY0) of 6.9x.

12.5x

EV/EBITDA (2021/22-05E)

Xeinadin Group is a leading UK and Ireland professional services group comprising approximately 100 business advisory and accountancy practices, offering over 40 service lines to more than 50,000 SME clients. The business is relevant in an accounting-services valuation context as a large-scale, buy-and-build accountancy consolidation platform with deep SME client penetration.

According to our analysis of Xeinadin BidCo Limited’s statutory accounts, Exponent Private Equity acquired Xeinadin Group Limited at an implied enterprise value of approximately GBP 375m. The company was marketed off an EBITDA of GBP 30m for FY2021/22-05E according to our sources, representing an EV/EBITDA (FY1E) of c. 12.5x at the time. Based on reported revenue of GBP 107m for FY2021/22-05R, the transaction also implies an EV/Sales (FY1R) of c. 3.5x.

11.0x

EV/EBITDA (2021-12R)

Citrin Cooperman is described in further detail in the January 2025 transaction entry above.

Prior to the January 2025 Blackstone-led acquisition described above, New Mountain Capital acquired a majority stake in Citrin Cooperman in October 2021 at an enterprise value of approximately USD 500 million and an EV/EBITDA (FY1) multiple of approximately 11.0x, according to reporting by established financial media at the time (The Financial Times, citing persons familiar with the matter). Net revenue for FY2021 was USD 351.8 million as reported by Inside Public Accounting, implying an EV/Sales (FY1) of approximately 1.4x.

8.3x

EV/EBITDA (2019/20-11R)

Rätinki-Yhtiöt is a Finnish accounting firm providing bookkeeping, accounting, and related professional services through a team of 31 professionals at the time of the transaction. The business is relevant in an accounting-services valuation context as a small-scale Finnish accountancy transaction, reflecting the valuation dynamics applicable to smaller, founder-owned accounting businesses acquired by listed consolidators participating in the ongoing fragmentation-driven consolidation of the Nordic accounting services market.

According to the transaction announcement at the time, Aallon Group – the Finnish publicly listed accounting firm – acquired Rätinki-Yhtiöt and its subsidiaries for a total consideration of EUR 3.3m. For the financial year ending 30 November 2020, the business reported revenues of EUR 2.3m and adjusted EBITDA of EUR 0.4m, reflecting an EV/Sales (FY0) of 1.4x and an EV/EBITDA (FY0) of 8.3x.

6.3x

EV/EBITDA (2019-12R)

Admit Ekonomi is a Swedish accounting firm providing bookkeeping, accounting, and related professional services to SME clients. The business is relevant in an accounting-services valuation context as a small-scale Swedish accountancy transaction, illustrating the lower end of the valuation range for smaller accounting businesses acquired amid the ongoing consolidation of the Nordic accounting services market.

According to the transaction announcement at the time, Stockwik Förvaltning acquired Admit Ekonomi for approximately SEK 31.3m. For the financial year 2019, the business had reported revenues of approximately SEK 30m and EBITDA of approximately SEK 5m, reflecting an EV/Sales (FY0) of 1.0x and an EV/EBITDA (FY0) of 6.3x.

2018

~2.1x

EV/Sales (2017-12R)

PwC Sweden’s Business Services division provided accounting, payroll, and related advisory services to SMEs in Sweden. The transaction is relevant as a large Nordic accounting-services carve-out that showed how Big Four-affiliated divisions could be separated and scaled as standalone platforms under private equity ownership.

According to reporting at the time, IK agreed to acquire the division for approximately SEK 2bn, while the business generated SEK 950m of revenue in 2017, implying an EV/Sales multiple of approximately 2.1x.

Across the analysed transactions, EV/EBITDA outcomes range from approximately 6x to the mid-teens, with most observed platform deals clustering around 9x–12x.

However, dispersion is structural rather than cyclical.

Broadly:

The key takeaway is that accounting services is not a homogeneous valuation category.

Size alone does not command a premium, nor does audit exposure by itself. Valuation appears to be driven primarily by platform quality: recurring client embedment, institutional depth beyond individual partners, technology-enabled delivery, and credible consolidation potential. In practice, the market pays less for “accounting” as a label than for evidence that the business can scale beyond a partner-led model.

Valuation dispersion in Accounting Services is driven less by the “accounting” label itself and more by differences in revenue quality, service mix, delivery model, and institutional scalability. In practice, buyers are underwriting the durability, transferability, and expandability of earnings, not just their recurring appearance on paper.

Key drivers typically include:

1. Revenue visibility and workflow criticality

Revenue tied to recurring, non-discretionary finance, tax, payroll, reporting, and assurance workflows is valued more highly than episodic or lower-touch work. The more operationally embedded the provider is in a client’s ongoing finance function, the stronger the defensibility and renewal visibility.

2. Service mix and pricing power

Not all accounting revenue is equal. Basic bookkeeping and routine compliance are increasingly standardised, while advisory, assurance, outsourced finance, and broader value-added support tend to carry stronger pricing power, deeper client ownership, and better cross-sell potential.

3. Technology enablement and delivery scalability

Technology matters when it changes delivery economics. Firms that use automation, workflow tools, and centralised processes to reduce manual work and improve consistency are typically more scalable, less partner-dependent, and better positioned to improve margins.

4. Institutional depth beyond individual partners

A core valuation question is whether the earnings belong to the firm or to individual partners. Businesses with stronger second-line leadership, standardised delivery, central functions, and more portable client relationships tend to underwrite better than firms where continuity depends heavily on a small number of rainmakers.

5. Buy-and-build credibility

Fragmentation creates opportunity, but only where the platform can actually consolidate it. Buyers pay more for firms with a credible ability to integrate acquisitions, standardise systems, centralise overhead, and add adjacent services across a wider base.

6. Regulatory and governance complexity, especially in audit

Audit can improve defensibility, but it can also complicate ownership and structuring. In several markets, audit firms must remain majority-controlled by qualified auditors, and regulators continue to emphasise audit quality, independence, and public-interest safeguards; as a result, audit exposure does not automatically command the highest valuation.

The key takeaway is that valuation in Accounting Services is driven less by sector label and more by platform quality.

The market pays most consistently for firms that combine recurring workflow embedment, higher-value service mix, scalable delivery, institutional depth, and credible consolidation potential.

The buyer universe in Accounting Services is led by financial sponsors, with selective participation from listed and strategic accountancy consolidators. Private equity activity has expanded rapidly across Europe and is increasingly targeting not only small local firms but also larger, multidisciplinary, and audit-exposed platforms.

Secondary buyouts and sponsor-to-sponsor transactions indicate that the consolidation thesis remains durable once a platform has achieved sufficient scale, integration capability, and institutional depth.

Despite broader M&A volatility, buyer interest in Accounting Services platforms has remained resilient. Consolidation is accelerating because four forces are converging at once: (1) persistent fragmentation, (2) rising succession pressure in partner-led firms, (3) growing technology and AI investment requirements, and (4) increasing demand for broader, ongoing finance and advisory support.

External capital is therefore solving not just ownership transition, but also scale, digitisation, and operating model change. Unlike more discretionary B2B services, demand remains anchored in recurring accounting, tax, payroll, and assurance workflows, which helps explain why deal activity has continued to expand. This is reflected in the sharp increase in European PE transactions in the sector since 2023, rising from 43 deals in 2022 to 192 in 2024, according to Accountancy Europe.

Subscriber edition

The Northern European Accounting Services landscape is characterised by a combination of sponsor-backed consolidation platforms, listed accountancy groups, strategic-owned assets, and a large base of privately held partner-owned firms. Private equity ownership has become increasingly visible in the sector, particularly across UK and Nordic buy-and-build platforms, while many mid-sized firms remain privately owned and continue to face succession, technology investment, and scale-related pressures.

Understanding this ownership landscape is relevant for assessing both current consolidation dynamics and the pipeline of potential future transactions. The chart and table below provide an overview of selected Accounting Services platforms across Europe, segmented by ownership type, service segment, revenue, and approximate EBITDA.

Revenue and EBITDA figures are approximate and partly from non-public sources. The figures predominantly relate to the financial year 2025 or 2024, with a few exceptions being 2026-03 figures.

Service segments as shown in the bubble chart (visible in the Subscriber Edition):

[TABLE WITH 39 ACCOUNTING SERVICES PLATFORMS IS AVAILABLE IN THE SUBSCRIBER EDITION ONLY]

[LIVE AND EMERGING OPPORTUNITIES ARE AVAILABLE IN THE SUBSCRIBER EDITION ONLY]

The following section highlights a selection of emerging M&A situations currently monitored by NKP | M&A Insights across the Northern European Accounting Services landscape.

Some of these situations remain pre-process or early-stage, meaning they may not yet be visible through traditional advisor-led market channels.

Company identities and transaction details have been intentionally blinded. The purpose of this section is not to disclose specific processes, but to provide forward-looking situational awareness around where consolidation activity is forming and how the opportunity landscape is evolving.

To retrieve additional context, including the names of the referenced companies - search for “accounting”, “accountancy”, or “payroll” (including the quotation marks) in the search field in Companies for Sale or contact us at research@mainsights.io for assistance.

Based on emerging situations currently being monitored across Northern Europe, several themes appear to be shaping the next phase of consolidation in Accounting Services.

A meaningful share of the current opportunity set consists of sponsor-backed accountancy platforms that have scaled through buy-and-build and are now approaching potential exit windows. This suggests that the next phase of activity is likely to include more secondary buyouts, continuation structures, and larger platform processes, particularly in the UK and Nordic markets.

The UK remains the most mature PE-backed consolidation market, but activity is increasingly spreading across the Nordics, the Netherlands, Belgium, Ireland, France, and Germany. As early UK platforms mature, larger consolidators are likely to look beyond domestic add-ons and use regional platforms as entry points into new European markets.

Partner succession remains a key catalyst, but broader operating pressures are increasingly reinforcing its importance. Smaller and mid-sized firms face rising talent shortages, higher technology investment needs, and growing demand for digital workflows, making larger platforms more attractive as both succession solutions and long-term operating environments.

Buyer appetite remains strongest for businesses with scale, management depth, recurring client relationships, technology-enabled delivery, and a broader advisory-led service mix. Basic bookkeeping, payroll, and compliance remain resilient, but premium valuations are more likely where firms can demonstrate pricing power, cross-sell potential, and reduced dependence on individual partners.

Audit and assurance capabilities can strengthen client embeddedness and strategic relevance, but they also introduce constraints on regulatory independence, governance, and ownership structuring. Buyer interest is therefore likely to remain strongest where audit exposure is combined with institutional scale, strong quality controls, and a structure that can accommodate external capital.

The 16 situations below represent a selection of emerging opportunities currently monitored within the Northern European Accounting Services landscape. These situations vary in maturity, ranging from early-stage strategic discussions to situations where more formal processes may emerge over time - company names and identifying details have been intentionally omitted.

[THIS SECTION IS ONLY AVAILABLE IN THE SUBSCRIBER EDITION]

Taken together, the emerging situations currently tracked across the Accounting Services landscape point to a market where consolidation remains structurally supported, but increasingly selective.

First, the sector structure remains highly favourable for consolidation. The market remains fragmented below the largest national and international networks, while many smaller and mid-sized firms face succession pressures, talent constraints, and rising technology investment needs. This creates a continuing supply of potential targets, but also widens the gap between institutionalised platforms and traditional partner-led practices.

Second, consolidation opportunities differ by market maturity. In the UK and other more developed markets, the most relevant opportunities are likely to be secondary buyouts, larger platform processes, and bolt-on acquisitions behind existing consolidators. In less consolidated European markets, there remains scope to build regional platforms around strong local firms with recurring SME relationships, local density, and limited internal capacity to fund technology and succession.

Third, valuation expectations should be anchored in platform quality, not sector exposure alone. Premium outcomes are most likely for businesses with scale, management depth, recurring client relationships, technology-enabled delivery, proven integration capability, and a broader advisory-led service mix. Smaller local practices remain attractive, but mainly as bolt-ons unless they bring clear niche expertise, local density, or differentiated client access.

Overall, Accounting Services consolidation is likely to remain active, but not indiscriminate. Financial sponsors and strategic buyers should both expect the most competitive processes to centre on assets that combine recurring compliance-led revenue with scalable delivery, credible buy-and-build potential, and a service mix extending beyond basic bookkeeping and compliance.

Valuation references in this analysis are indicative and reflect NKP | M&A Insights’ assessment of historical transactions based on publicly available information at the time of writing, including statutory accounts, regulatory filings, credit rating agency reports, sponsor materials and company press releases.

Where enterprise values are not explicitly disclosed, they are derived from disclosed consideration, debt assumptions, or implied values in transaction vehicles (e.g. BidCo / TopCo entities), cross-checked against available filings.

EBITDA figures reflect the metric referenced at the time of marketing where identifiable (e.g. adjusted EBITDA), or NKP’s assessment based on the most recent published annual accounts.

For clarity:

Where forward EBITDA was used in marketing materials, multiples are presented on an FY1 basis. Where historical accounts were the primary reference, multiples are presented on an FY0 basis. The basis applied is specified in each transaction summary.

In certain cases, EBITDA may reflect normalisation adjustments or full-year effects of completed acquisitions where such information was clearly disclosed. These adjustments reflect NKP’s assessment and may differ from buyer-underwritten figures.

Where precise figures are unavailable, ranges or approximations are used based on best available sources. All valuation references should therefore be interpreted as directional indicators rather than definitive transaction terms.

Supporting detail and transaction backup materials are available to NKP subscribers.

This report has been prepared by NKP | M&A Insights for informational purposes only. While NKP | M&A Insights has taken reasonable care to ensure that the information contained herein is accurate and based on reliable sources at the time of publication, no representation or warranty, express or implied, is made as to the accuracy, completeness, or timeliness of the information.

The analysis, views and conclusions expressed in this report reflect NKP | M&A Insights’ interpretation of publicly available information and proprietary intelligence sources and may be subject to change without notice.

Nothing in this report constitutes investment advice, an offer to sell, or a solicitation to buy any securities or assets. NKP | M&A Insights shall not be held liable for any direct or indirect loss arising from the use of, or reliance on, the information contained in this report.

This report is intended solely for the use of NKP subscribers and may not be reproduced, redistributed, or circulated without prior written consent from NKP | M&A Insights.

Download as PDF

Download as PDFWhether you are exploring a subscription or would like to discuss a situation relevant to our coverage, you are welcome to contact us directly.